Luxury and premium homes are a demand in the Pune residential market. The real estate market in the city is witnessing a clear structural evolution. The traction in the premium and mid-sized housing demand is more than the low-segment houses. The shift marks not just a cyclical upswing, but what industry experts describe as a structural premiumisation of Pune’s real estate landscape.

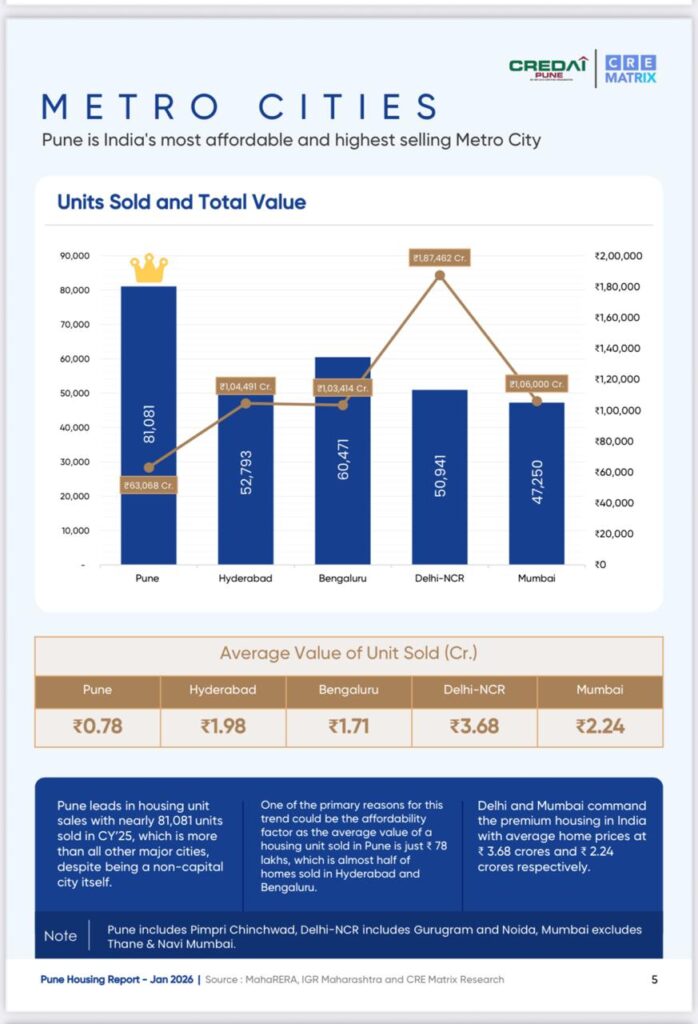

According to the Pune Housing Report by CRE Matrix, the demand for premium homes saw a spur in the CY 2025 and most of these homes are priced above ₹ 1 Crore. The city recorded the sale of over 81,000 housing units valued at more than ₹ 63,000 Crore, based on actual IGR registered sale deeds of new homes, excluding bookings and resale transactions. As compared to 2021, nearly 19% increase is observed in units sold and over 71% growth is reported in transaction value.

The rise of ₹ 1 crore plus segment

While the transaction volumes remain robust, buyer preferences are moving towards larger homes and higher value offerings, reflecting rising aspirations and income profiles. In CY 2025, 14,000 homes in ₹ 1-2 crore segment have been sold and 3,300 homes priced above ₹ 2 crore were sold. This represents dramatic growth since 2021. Under the ₹ 1-2 crore category the sales have grown nearly fourfold, while the ₹ 2 crore plus segment has expanded by about threefold, reflecting a clear trend in high-value home buying.

The average ticket size in CY 2025 was recorded ₹ 78 Lakh, marking a 44% growth over the last five years, driven by larger home sizes and rising per-square-foot values. As developers pivot toward bigger homes and as land and compliance costs rise, the overall value of transactions has climbed significantly.

Abhishek Kiran Gupta, CEO, CRE Matrix while talking about the premiumization cycle says, “In recent years developers have increasingly focused on larger configurations such as 3 and 4 BHK homes, primarily because affordable housing projects have become financially challenging to execute. At the same time, many buyers who purchased homes in Pune 10-15 years ago are now looking to upgrade to bigger homes. These factors together have led to an increase in both apartment sizes and ticker values. This trend clearly represents a classic premiumization cycle, typically observed as cities evolve from developing to a more mature real estate market.”

Affordability: Pune’s enduring advantage

Yet, even as premium housing surges, Pune continues to be the most affordable housing market among the Indian metros, with average home prices significantly lower than Mumbai which has a cost of ₹ 2.2 crore, Bengaluru ₹ 1.71 crore, and Hyderabad ₹ 1.91 crore, despite it records the highest housing unit sales in the city.

“Pune’s market continues to function on free-market principles, and developers recognise that nearly 80% of transactions occur below ₹ 1 crore price point. Consequently, a large share of ongoing development continues to cater to this segment. Pune is likely to retain this advantage, while cities with significantly higher average ticket sizes may begin to experience slower absorption, as such price levels can discourage new homebuyers. Over the next five to ten years, Pune’s relative affordability is expected to continue attracting migration and housing demand, reinforcing its competitive advantage,” informs Gupta.

Changing buyer preferences: bigger homes, bigger ambitions

Data from CREDAI underscores the shift in homebuyers preferences. The unit sales of 3 and 4 BHK homes grew to 29% from 20% and the demand for 1 BHK homes in new launches has moderated from 18% to 11%. As a result the average size of newly launched homes in Pune has increased by 17% over the past five years.

This clearly shows that the preference of home buyers has moved to larger apartments and nearly 78% of homes sold during 2025 were priced below ₹ 1 crore. Affordability and premiumization is the only factor that Pune’s real estate market is relatively affordable than the other metros in India.

Asked if this demand is driven by higher incomes, or investor demand or lack of supply in lower price bands, Gupta shares, “The primary driver has been the rising income, particularly among the IT professionals who witnessed strong post-covid salary growth, with many also taking up multiple income opportunities. Higher buyer incomes naturally translate into higher purchasing power, which supports price growth. At the same time, supply in the lower price segment remains limited, compelling many households to delay purchases and continue renting. Investor demand was significant immediately after covid, but it has moderated in recent years.”

Micro-markets: divergence within the city

Despite the city having recorded premium growth, nearly 78% homes are still sold below ₹ 1 crore. Pune is uniquely balancing affordability and aspirations. “Pune operates largely as a free market where developers choose to build products that are financially viable. Since demands for homes priced ₹1 crore remained strong, developers continued to build in emerging corridors such as Punawale, Tathawade, parts of West Pune and Wagholi in East Pune. However, affordability is gradually eroding in established micro-markets such as Baner, Balewadi and Kharadi, where finding a good quality 2-BHK below ₹ 1 crore is increasingly difficult, and well sized 3-BHK homes in prime location often exceeds ₹ 2 crore. As a result many buyers are now moving slightly further out to access more affordable options,” informs

Rahul Ajmera,

Pune based developer and data expert

As per the report by CREDAI, Central Pune’s average ticket size has already crossed ₹ 1.35 crore, with 74% unit growth since 2021. “Central Pune commands high ticket sizes mainly because developments are concentrated in small, premium micro markets like Shivajinagar and Koregaon Park, where supply is limited and traditionally affluent communities are concentrated. Premiumization may extend to a few additional micro-markets such as Baner, Kharadi and Mundhwa. However, it is likely to spread across the city at the same pace, as affordability remains a key consideration. Developers are cautious about shifting too aggressively toward premium products since doing so could affect sales velocity,” explains Gupta.

Regulatory bottlenecks and supply constraints

Despite Pune seeing a sharper increase in the sales of the units sold in the CY 2025, yet the volumes of these units dropped nearly 12-15%. Last year environmental clearance and approvals in PMC, PCMC, PMRDA and the surrounding 5-km radius were temporarily stalled, followed by delays and demarcation approvals, which led to a lower number of project launches in Pune.

“The decline in volumes is largely linked to subdued new project launches over the past few years, mainly due to regulatory challenges such as delays in environmental clearances and land demarcation approvals. As a result, reduced supply has translated into lower sales volumes. This situation reflects structural constraints in approvals rather than a weakening of underlying buyer demand,” shares Ajmera.

Despite these short-term supply side challenges, Pune district continues to lead the country in regulatory activity, with the highest number of MahaRERA registered projects and agents in India. The district has consistently recorded over 1,000 new projects registrations annually since 2021, underscoring strong and sustained developer confidence in the market. “With time, as the industry is getting more organised, we are seeing significantly larger development and township projects which are bringing in bulk of the inventory. Yes, there are smaller developments as well but they are contributing to a lesser number of inventories in the market,” says

Manish Jain, President CREDAI.

As per the report, developers launched 64,000 new units in 2025 against 81,000 registrations, which means that the potential supply was delayed due to environmental clearance and demarcation approval. Ask the reason from Manish behind this demand supply gap, he explains, “Usually developers were launching 90k to 1 lakh units regularly post covid. This has gradually slowed down because real estate is cyclical. But 64,000 is an approximate slowdown, so maybe about 15,000-20,000 units were probably delayed due to these issues.”

Environmental clearances, regulatory delays are the causes of delay in the new launches. This will cause a lot of projects to become unviable if the delay persists for a longer period of time. To compensate for this developers will be forced to bring in inventory at a higher price point, which will erode affordability in the market for everyone. “The demand has gradually slowed down because it is cyclical. Once the prices go up, the demand also tends to go down. But since there are so many jobs being created in Pune, we don’t see a problem with any significant slowdown of demand,” feels Manish.

“The infrastructure is a main point in Pune. Things are happening, the outer ring road is happening, the metro construction is ongoing. However, there are some very critical infrastructure issues such as missing links in DP roads and water supply projects, and STPs and water sewage projects that really needs to be taken on a warfooting, because significant parts of Pune still do not have good connectivity by roads, neither do they have water supply from municipal corporations. This needs to be fastracked at the earliest,” Manish adds.

Structurally stronger cycle

The CREDAI report indicates that the transaction value fell only by 6% from peak levels but the volumes dropped 12-15%. Does this signal a structurally stronger buyer base compared to the pre-2020 cycle? “The decline in volumes is largely linked to subdued new project launches over the past few years, mainly due to regulatory challenges such as delays in environmental clearances and land demarcation approvals. As a result reduced supply has translated into lower sales volumes. This situation reflects structural constraints in approvals rather than a weakening of underlying buyer demand,” answers Ajmera.

The MahaRERA new launches report January 2026, highlights a clear shift in developer strategy towards larger homes. Where 3-4BHK units sold went up to 29% from 20%, the 1 BHK launches fell to 11%. This evolving homebuyers’ preferences is both demand-led and driven by economics. “The demand for 1 BHK is gradually reducing as homebuyers prefer larger homes. Incomes have also risen sharply in the last 10-15 years. Also, it is no longer affordable for developers to build 1 BHK homes, as land prices have become so expensive and the cost of doing business due to the various hurdles while doing the business is a lot. It takes a very long time, from the time you buy the land till when the project is launched. So, all this adds to a significant inflation in the cost, and hence it is not affordable to do projects where the margins are very less,” says Manish.

Even the change in buyers’ demand has also been observed between 2021-2025. “Immediately, after covid, investor activity surged as property prices appreciated sharply, offering strong returns. However, as price growth moderates, investor interest is gradually mornalising. Meanwhile, upgrader demand has increased significantly, with many households moving from long-held 2BHK homes to larger 3-4BHK units. Additionally, first-time buyers are also opting for larger homes than before. Earlier, first-time purchases typically involved 1 or 2 BHK units, whereas today many first-time buyers are directly choosing 2.5 or 3 BHK configurations,” says Ajmera.

“When you are building homes that are priced less than ₹ 50 Lacs, they are usually a compact 1BHK or 2BHK and they are more into the affordable market. To make unit economics work, one needs affordable cost of construction, lesser taxation and affordable land prices. Unfortunately, it is no longer viable in 2026 for this segment, and the government will have to provide some incentives such as income tax exemption or reduction in GST and stamp duty to make housing truly affordable below this price point. It was affordable 10 years back but it is no longer affordable today,” says Manish.

Since the environment clearances and regulatory demands are the cause of delays, if these get normalise in 2026, the demand and supply may balanced out “If approvals are streamlined in 2026 given that it is still taking significantly long after buying land, I think it will take at least one year before new supply hits the market. So the one year and three year correction cycle will get balanced out,” feels Manish.

Echoing the same sentiments, Ajmera shares, “If approvals improve and supply increases, it should lead to higher sales in currently underserved areas and help stabilize prices. Ideally, pent-up demand should be able to absorb the new supply, preventing any sharp correction in prices while maintaining market stability.”

Pune’s residential market is no longer merely an affordable alternative to larger metros. It is evolving into a mature, aspirational housing destination where premium products coexist with a broad affordable base. Rising income, changing buyers preferences, constrained land supply and regulatory bottlenecks, have collectively pushed the market into a premiumisation cycle. Yet, the city’s comparative affordability continues to attract migration and sustained demand.

Ultimately, Pune is transitioning from a volume-driven affordable housing market to a value-driven premium housing cycle.